CSRD: What It Is and How It Will Impact Brazilian Companies (and Any Company Outside the EU)

By David Muñoz Blanco *

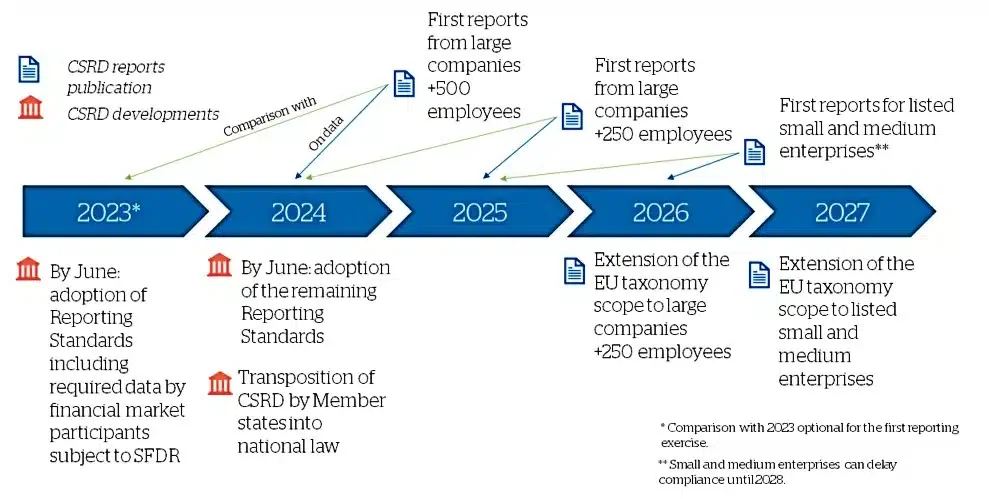

As of January 1, 2024, European-based companies already adhering to the NFRD (Non-Financial Reporting Directive) will need to comply with the CSRD (Corporate Sustainability Reporting Directive), the EU's new directive for corporate sustainability reporting. After 2024, the cascade effect begins for medium-sized and small companies and foreign companies with operations in the EU.

Increasing transparency and uniformity of ESG information for all stakeholders (from investors to society at large) to facilitate the transition to a more sustainable and decarbonized economy: this is the main goal of the CSRD.

Among the changes introduced by the new directive are:

-

Expanded applicability to more companies (from 12,000 to 50,000), now including small and medium-sized enterprises and foreign companies with operations in Europe.

-

Introduction of double materiality (considering both the impact of climate change on companies' financial health and the impact of companies on the environment and people – previously, under the NFRD, only financial materiality was mandatory).

-

Consolidation of double materiality through the new ESRS: European Sustainability Reporting Standards, harmonizing different market standards into one.

-

Inclusion of indirect emissions (scope 3) and the mandatory requirement for a decarbonization plan throughout the value chain of companies according to ESRS (EU Sustainability Reporting Standards).

-

Mandatory audit – previously voluntary for the entire European bloc and mandatory only in some countries.

-

Standardized format (xHTML with XBRL technology) for integrated reporting (single reporting, combining financial and sustainability information). XBRL technology standardizes and makes information comparable according to the EU taxonomy. Thus, each item is accounted for and calculated in the same way for all companies, from all countries in the bloc (this format may only become mandatory from 2025).

How will the CSRD impact Brazilian companies and those outside the EU?

Starting in 2024, all Brazilian companies that are subsidiaries of European companies affected by the CSRD will need to provide their ESG information according to ESRS standards. All Brazilian companies that are suppliers or clients of European companies will need to demonstrate how their carbon inventory fits into the decarbonization plan of the European company to which they are linked via scope 3.

Furthermore, from 2028, all companies headquartered outside the EU with a net revenue exceeding 150 million euros and a subsidiary in the bloc will need to report (not just provide information) in accordance with the CSRD and ESRS.

There is a strong alignment between ESRS and IFRS S1 and S2, which are sustainability disclosure standards established by the ISSB (International Sustainability Standards Board) and have been adopted in Brazil in November of this year. This will facilitate the adaptation of Brazilian companies to European standards.

Brazilian companies that operate, do business, or receive investments in Europe should proactively organize their information according to ESRS standards and have a decarbonization plan regarding their GHG inventory. This way, they can develop a competitive advantage over others and avoid interrupting their activities in the EU.

Fonte: European Commission

* David Muñoz Blanco is a consultant at DEEP with extensive experience in financial and sustainability reporting, having worked with major consulting firms and corporations in the European Union, South and North Americas, and Africa.